Nvidia ($NVDA) has been the star of Wall Street, especially with its growth in AI and astonishing performance. However, there are strong reasons to consider Intel ($INTC), Samsung ($SSNLF), and TSMC ($TSM) as even better investment opportunities. The semiconductor landscape is changing, and these companies are well-positioned to benefit. From the slowing of Moore’s Law to the power of owning fabs, Intel, Samsung, and TSMC have unique advantages that could outshine Nvidia’s prospects and make them better investments. Here are five reasons why they might be your best bet.

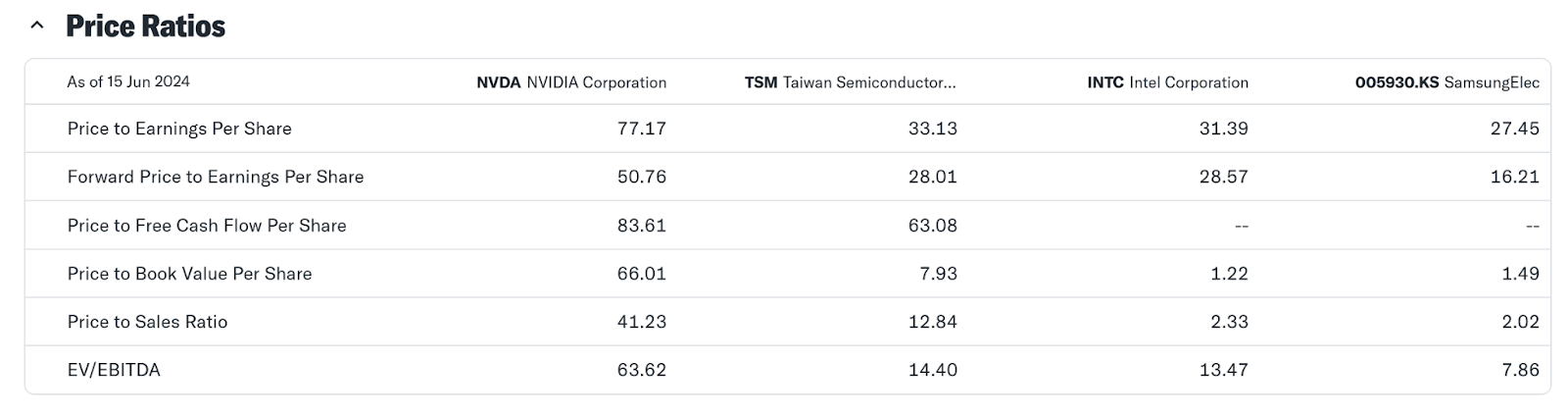

1. Valuation Matters

Nvidia’s current high valuation reflects its market success in AI, but this also means that this success is already priced in, which reduces the upside potential. It is true that in the very long run, a company with a Return on Equity (ROE) of 20% will produce a similar return for its stock. Multiple expansion, such as Price to Earnings (P/E) or Price to Sales (P/S) re-rating, is a one-off event. A P/E of 5 can rise to 20, or a P/E of 10 can rise to a bubbly 40, providing a nice 4x return. However, this expansion isn’t sustainable in the long term. What can be sustainable or not, is the earnings growth part.

So some of Nvidia’s recent great return is due to multiple expansion (re-rating), and some of it is due to real earnings growth. If real earnings growth continues at the same pace, this is definitely a tailwind. But you have to be aware that multiple expansion, while it is sweet at present, is a headwind for future returns.

On the contrary, Samsung, TSMC and Intel are not growing as fast as Nvidia, but they have more room for positive re-rating. Additionally, as we will see later, their growth is modest but likely more sustainable, and probably able to accelerate.

2. Earnings Cycles

The semiconductor industry is inherently cyclical. While Nvidia is already enjoying a favorable earnings phase, Intel, Samsung, and TSMC are still in the downcycle. This phase can be advantageous for investors who buy at lower valuations, positioning themselves for significant gains when these companies recover and enter their upcycle phase. Historically, semiconductor companies have shown robust rebounds following downcycles, making strategic investments during these periods particularly lucrative.

Nvidia was the first to break out of this cycle for reasons explained in the next section, but the rest haven’t yet. The graph below, showcasing the operating margins of Samsung, TSMC, Intel, and Nvidia, illustrates this. Big earnings can be ahead, as the rest will follow with some latency.

3. Impact of small AI segments on Revenue

Nvidia’s revenue is predominantly driven by AI. In contrast, Intel, Samsung, and TSMC have smaller exposure in AI for the moment. For example, TSMC currently derives about 10% of its revenue from AI-related business. If this segment continues growing by 50% annually for a few years, AI could constitute a significant portion of TSMC’s total revenue. As the AI segment continues to expand and becomes a larger part of the overall revenue mix, its impact will be increasingly significant.

This dynamic is similar to the transformation seen in other companies with growing and stagnant segments. Initially, the growing segment is too small to be noticed, but as it grows larger, its influence on overall revenue becomes substantial, potentially driving dramatic growth in the company’s financial performance.

Nvidia is already heavily focused on AI, so we should not expect further acceleration in its growth pace. However, TSMC, Intel, and Samsung are poised to increase the AI component of their revenue, which promises significant growth acceleration in the future.

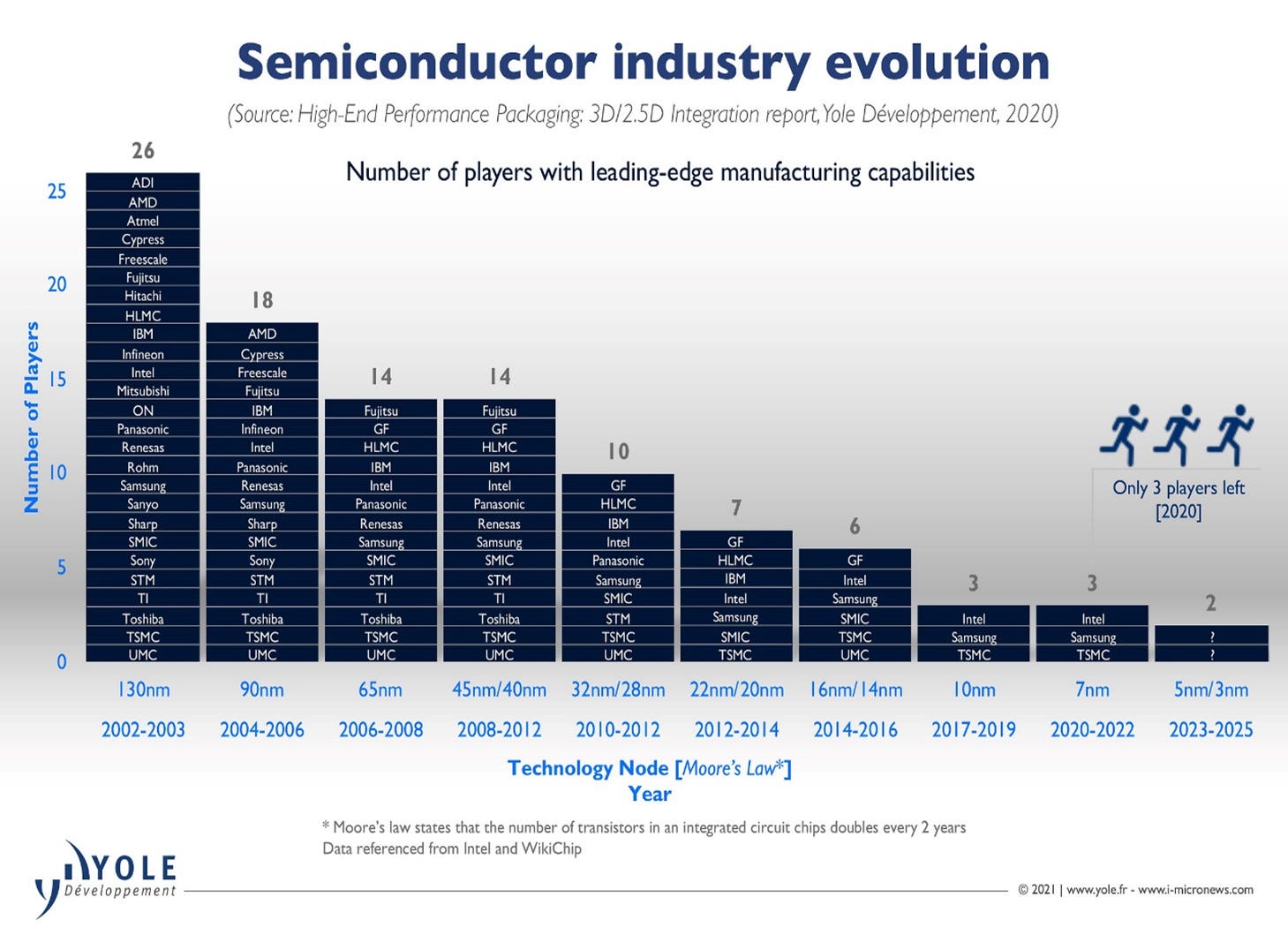

4. Real Fabs versus fabless Nvidia

Intel, Samsung, and TSMC have fabrication capabilities, whereas Nvidia is fabless. Leading-edge manufacturing is an extremely complicated process that demands substantial research and investments. From this brutal multi-year competition, only three companies in the world can still manufacture the chips that Nvidia or any other accelerator needs (such as AMD, Groq, Cerebras, Google, Amazon, etc.).

So far, through CUDA and the overall Nvidia ecosystem, the company acts as a monopoly, which protects its margins. However, AMD and other players are catching up and will all compete for the limited production of top-edge chips that only Intel, TSMC, and Samsung can offer.

As Nvidia competes with other players, the fabless space will get commoditised, and the margins will shift to the source, namely the fabs. Recently, TSMC’s new Chairman, Mark Liu, remarked, “I did complain to Nvidia’s CEO Jensen Huang — the ‘three trillion guy’ — that his products are so expensive. I think those products are really valuable for sure, but I am thinking about showing [him] our values as well” .

The dynamics will favour the fabs, which will finally capture the hefty margins currently enjoyed by Nvidia, as the latter relies on them.

5. The Slowing of Moore’s Law

What adds to the previous argument is the slowing of Moore’s Law, which predicts the doubling of transistors on a microchip approximately every two years. As this trend decelerates, there is increasing pressure for greater chip manufacturing capability, making it more expensive, challenging, and scarce.

If you take the greatest fabless chip producers (Nvidia, AMD, etc.) and see the performance of their products at older, less dense nodes, you will realize the dramatic role that underlying silicon density plays. This is why older chips become almost useless.

As manufacturing becomes really hard and is controlled by these three players (TSMC, Intel, Samsung), the fabless manufacturers will almost become hostages to these companies and their miraculously complicated operations.

Summing Up

In conclusion, while Nvidia’s achievements in AI are notable, Intel, Samsung, and TSMC offer compelling reasons for investment. Their attractive valuations, strategic positioning in the earnings cycle, diversified revenue streams, robust fabrication capabilities, and ability to navigate the slowing of Moore’s Law make them promising long-term investment opportunities in the semiconductor industry.

The cyclical phase differences, revenue dynamics, real fab nature, and the slowing of Moore’s Law are factors that promise some acceleration in growth for TSMC, Intel, and Samsung. These factors also suggest that Nvidia’s growth may slow down. Additionally, valuation matters, making these other companies attractive investment alternatives compared to Nvidia.

Disclaimer: The author owns TSMC, Samsung, and Intel shares.

Other semiconductor stocks owned: Micron, ARM, Qualcomm, ASML

*Content presented on FinAI does not present any recommendation for stock transactions. All investors are advised to conduct their own independent research into individual stocks before making a purchase decision.

Discover more from FinAI

Subscribe to get the latest posts sent to your email.

Dim

https://finance.yahoo.com/news/tsmc-shatters-records-ai-boom-124104173.html

TSMC is partying!